Supply Levels Improve in January

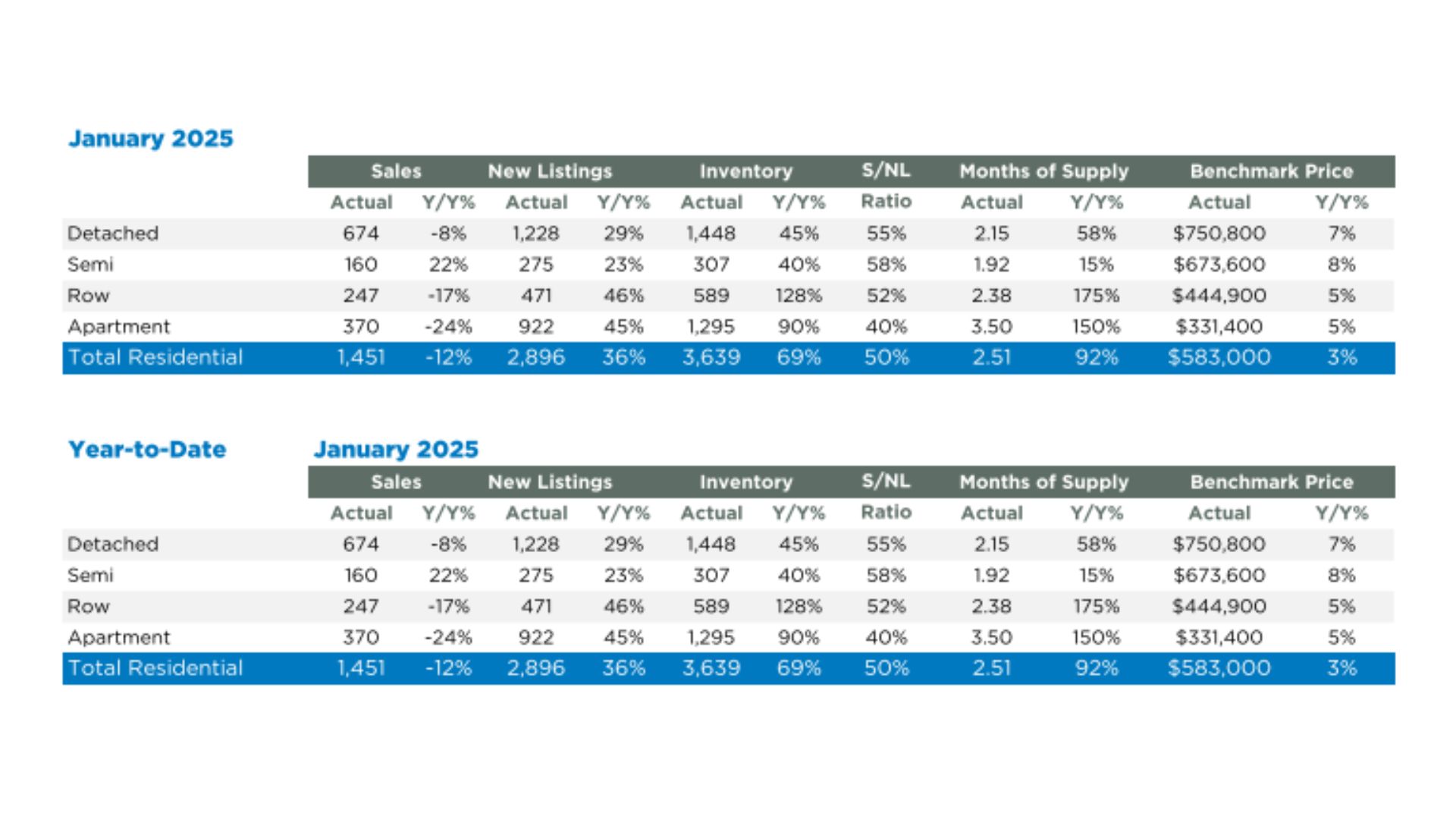

Calgary, Alberta – February 3, 2025 – After three consecutive years of limited housing supply, January saw a notable improvement in inventory levels, rising to 3,639 units. This 70% year-over-year increase is substantial, yet inventory remains below the typical January average of over 4,000 units. The most significant gains were seen in apartment-style condominiums.

“Supply levels are expected to improve this year, contributing to more balanced conditions and slower price growth,” said Ann-Marie Lurie, Chief Economist at CREB®. “However, the adjustment in supply is not equal across all property types. Detached, semi-detached, and row properties continue to experience tight conditions, while apartment condominiums are seeing excess supply in higher-priced segments.”

Despite the increase, citywide months of supply reached only 2.5 months in January—an improvement from last year’s single-month supply but still low for the winter season. Semi-detached properties saw the lowest months of supply at under two months, whereas apartment-style units had the highest at 3.5 months.

The increase in supply was driven by new listings, which rose to 2,896 units, compared to 1,451 sales. January sales were down 12% from last year but remained nearly 30% higher than the typical January average.

The total residential benchmark price for January stood at $583,000, a stable figure compared to the end of 2024 and nearly 3% higher than last January. Price growth varied across city districts and property types.

January 2025 Housing Market Breakdown

Detached Homes

New listings for detached homes reached 1,228 units in January, up 29% year-over-year, driven largely by homes priced above $600,000. Sales activity declined to 674 units, bringing levels in line with long-term trends. While inventory gains improved conditions, available stock (1,448 units) remains 27% below historical January averages, keeping the months of supply at just over two months.

Market conditions varied across districts, with the City Centre and North East districts experiencing more balanced conditions. The unadjusted benchmark price rose to $750,800, a slight monthly increase and 7% higher than January 2024. Seasonally adjusted prices have remained stable since mid-2024.

Semi-Detached Homes

Increased new listings helped bolster inventory levels in this sector. Sales in January outpaced last year’s levels, maintaining a months-of-supply ratio just below two months. However, supply conditions varied, with the City Centre, North East, and West districts reporting three or more months of supply, while other districts remained below two months.

The unadjusted benchmark price stood at $673,600, slightly lower than December but over 8% higher than January 2024. Districts with higher months of supply experienced modest price declines, while North, North West, South, South East, and East districts saw stable to moderate price gains.

Row Homes

In 2024, row home sales reached 4,647 units—a 2% increase from 2023—marking the second-highest total on record. New listings rose by 18%, primarily in homes priced above $400,000, leading to improved inventory levels.

Supply improvements eased price pressure towards the end of 2024, though annual benchmark prices still rose 14%. Price increases were citywide, ranging from 12% in the City Centre to over 20% in the most affordable areas of the North East and East districts.

Apartment Condominiums

January saw a surge in new listings compared to sales, causing inventory to rise to 589 units—more than double the near-record lows of January 2024. This brought inventory levelsels closer to long-term trends and improved the months of supply to over two months, a trend seen since mid-2024.

Rising supply eased price pressures, but price movements varied by district. The citywide unadjusted benchmark price stood at $444,900, down slightly from December but nearly 5% higher than last year. The North East district saw the most significant monthly price adjustment.

Regional Market Overview

Airdrie

Sales in January remained consistent with last year’s high levels, while new listings increased, boosting inventory levels. The months of supply remained above two months for the fifth consecutive month, a significant improvement from the sub-two-month levels seen since 2021. The unadjusted benchmark price declined slightly from December to $537,300 but remained nearly 4% higher than January 2024.

Cochrane

Cochrane experienced an increase in new listings and inventory, with 104 new listings compared to 71 sales, pushing total inventory to 156 units. While inventory is higher than in the past three years, it remains below long-term January averages. For the fifth consecutive month, Cochrane’s months of supply remained above two months, reducing price pressures. The unadjusted benchmark price was $565,900, a slight monthly decline but nearly 5% higher than January 2024.

Okotoks

Unlike Airdrie and Cochrane, new listings in Okotoks remained relatively low compared to last year. While lower sales supported some inventory growth, available stock (68 units) is still half of pre-pandemic January levels. Limited supply has driven price growth since 2021, with January’s unadjusted benchmark price rising to $614,900, up slightly from December and nearly 5% higher than January 2024.

For full City of Calgary and regional statistics, visit the official CREB website.